Property taxes can make a significant difference in your total cost of homeownership. Here’s what every homeowner and homebuyer should know about how property taxes work, how they’re paid, when they’re due, and their impact on your mortgage.

How Are Property Taxes Calculated?

Property taxes are calculated by multiplying the assessed value of your property by your area’s mill rate (tax rate). The assessed value is determined by your local tax assessor and may not match your home’s market value.

Formula:

How Do Rates Vary?

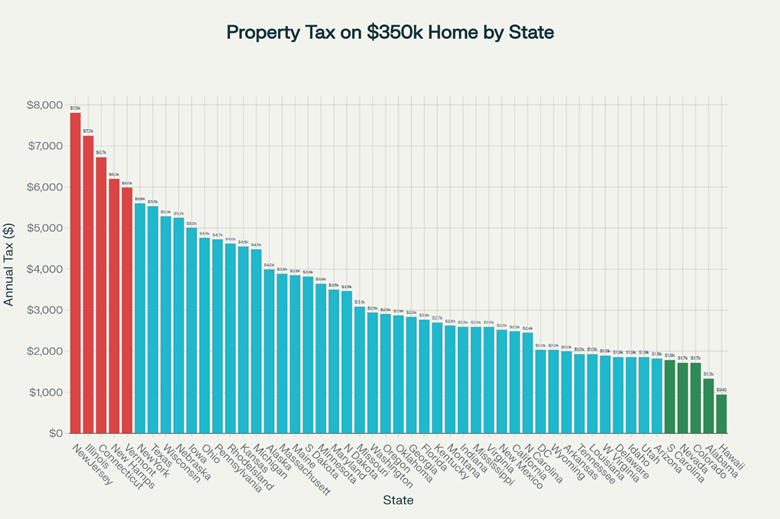

- Highest rates: New Jersey, Illinois, Connecticut, New Hampshire, Vermont

- Lowest rates: Hawaii, Alabama, Colorado, Nevada, South Carolina

Other factors:

- Assessment ratios and mill rates change by state.

- Assessments can be annual or triggered by ownership change/renovation.

- Exemptions: veterans, seniors, disabled, and homestead owners may qualify for relief (details vary by state).

Affordability Impact

- Higher property taxes increase your monthly payment and affect qualifying for loans.

- Lenders often include property taxes in your mortgage escrow.

Are Property Taxes Deductible?

Yes, your property taxes are deductible on your federal income tax return (up to limits set by the IRS). This deduction can help lower your overall tax bill and increase the affordability of homeownership for many buyers.

Do Property Taxes Go Up or Down?

More often than not, property taxes increase over time as assessed values rise or community budgets expand. However, taxes may go down if:

- The market value of your home drops,

- You qualify for exemptions (such as for seniors, veterans, or primary residences),

- You successfully appeal an inflated assessment.

Are Property Taxes Included in a Mortgage?

For most homeowners, yes! Property taxes are included in your monthly mortgage payment and held in an escrow account by your lender. This ensures your taxes (and often homeowners insurance) are always paid on time.

If you don’t escrow, you’ll pay taxes directly when billed by your local assessor.

Annual Property Tax by State on a $350,000 Loan (2025 Rates)

Check how much you might pay in every state with the chart below:

Annual property tax on a $350,000 loan by US state (2025 rates)

When Are Property Taxes Due?

Due dates vary by state and county. Some areas bill annually, while others collect payments twice a year or quarterly. Always check with your local tax assessor’s office for exact deadlines to avoid penalties or interest charges.

- Alabama: December 31 (statewide)

- Alaska: Varies by jurisdiction (county by county)

- Arizona: 1st half due November 1, 2nd half due May 1 (statewide)

- Arkansas: 1st half due April 16, 2nd half due July 15 (statewide)

- California: 1st half due December 10, 2nd half due April 10 (statewide)

- Colorado: 1st half due last day of February, 2nd half due June 15, or full by April 30 (statewide)

- Connecticut: 1st half due July 1, 2nd half due October 1 (statewide)

- Delaware: September 30 (county by county)

- Florida: March 31 (statewide)

- Georgia: 1st half due September 15, 2nd half due November 15 (county by county)

- Hawaii: 2nd half due February 20, 1st half due August 20 (county by county)

- Idaho: 1st half due December 20, 2nd half due June 20 (statewide)

- Illinois: 1st half due June 1, 2nd half September 1 (county by county)

- Indiana: 1st half due May 10, 2nd half November 10 (statewide)

- Iowa: 1st half due September 30, 2nd half March 31 (statewide)

- Kansas: 1st half due December 20, 2nd half May 10 (statewide)

- Kentucky: 1st half due November 30, 2nd half February 28 (county by county)

- Louisiana: December 31 (county by county)

- Maine: Varies by jurisdiction (county by county)

- Maryland: September 30 (county by county)

- Massachusetts: Quarterlies—Feb 1, May 1, Aug 1, Nov 1 (statewide)

- Michigan: Summer bills due July–September, winter bills due Dec–March (county by county)

- Minnesota: 1st half due May 15, 2nd half due October 15 (statewide)

- Mississippi: 1st half due August, 2nd half by December (county by county)

- Missouri: December 31 (statewide)

- Montana: 2nd half due May 31, 1st half due November 30 (statewide)

- Nebraska: 1st half due April 30, 2nd half due August 31 (statewide)

- Nevada: 1st, 2nd, 3rd, 4th installments—Aug, Oct, Jan, March (county by county)

- New Hampshire: 1st half due July 1, 2nd half due December 1 (statewide)

- New Jersey: Quarterly—Feb 1, May 1, Aug 1, Nov 1 (statewide)

- New Mexico: 1st half due November–December, 2nd half due April–May (statewide)

- New York: Varies by town/city (county by county)

- North Carolina: September 1 (statewide, but not delinquent until January 6 next year)

- North Dakota: 1st half due March 1, 2nd half October 15 (statewide)

- Ohio: 1st half due January–March, 2nd half June–August (county by county)

- Oklahoma: 1st half due December 31, 2nd half March 31 (statewide)

- Oregon: 1st third due November 15, 2nd third February 15, last third May 15 (statewide)

- Pennsylvania: Varies by jurisdiction (county by county)

- Rhode Island: Varies (county by county)

- South Carolina: January 15 (county by county)

- South Dakota: 1st half due April 30, 2nd half October 31 (statewide)

- Tennessee: February 28 (statewide)

- Texas: January 31 (statewide)

- Utah: November 30 (county by county)

- Vermont: Varies by jurisdiction (county by county)

- Virginia: May 1 (county by county)

- Washington: 1st half due April 30, 2nd half October 31 (statewide)

- District of Columbia: 1st half due March 31, 2nd half September 15 (statewide)

- West Virginia: 1st half due September 1, 2nd half March 1 (statewide)

- Wisconsin: January 31 (statewide, some municipalities allow installments)

- Wyoming: 1st half due November 10, 2nd half May 10 (statewide)

For states or areas that list “county by county,” check your local tax authority’s website for specific due dates.